Cheap Car Loan In Singapore

March 20, 2022

10 Cheap Motorcycle Loan In Singapore

April 15, 2022

Cost of Owning A Car In Singapore 2025

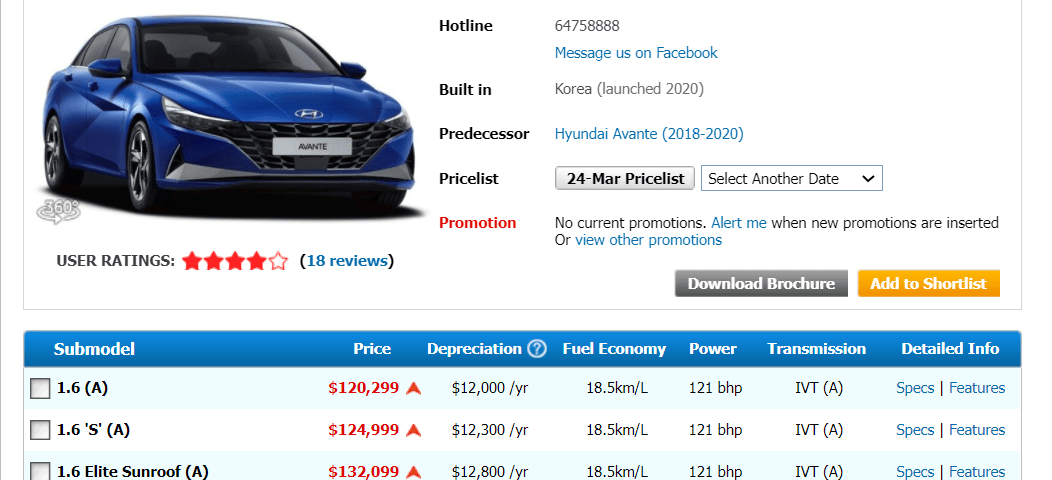

At some point in our lives, thoughts of owning a vehicle will definitely cross your mind, due to the added convenience or family needs. In Singapore, apart from the increased taxes levied from the Open Market Value (OMV), the COE system drastically increases the price of the vehicle, often costing way more than the actual price itself. For instance, the 2022 Hyundai Avante at its base trim costs just under S$30,000 in the US, but costs a whooping S$120,000 based on today’s COE prices (Mar 22, 2nd Bidding).

With such an outrageous price tag, potential owners often look to auto financing in order to increase affordability, paying a monthly instalment over a tenure of your choice.

For most people, if you are buying from an AD(Authorized Dealer) or other Car Dealers, they will usually have their own credit team to assists you with your vehicle loan applications. However, for people who are looking to purchase a car from a direct owner, you might not have access to these avenues, so we are here to help!

Vehicle Financing (Hire-Purchase)

BANK LOAN

Most of our local banks in Singapore are offering low interest rates starting from 1.88% onwards to entice potential vehicle owners to take up a vehicle loan with them, which seems to be the de-facto choice for some.

However, Banks will typically only loan you up to 70% of the vehicle price, depending on its OMV, meaning you will have to down-pay at least 30%, which can be quite a huge sum considering a brand new car will at least set you back by S$100,000.

Despite that, in terms of the interest, it is lowest amongst the various loan categories, incurring the least interest charged over the years.

In-House Credit/Finance Companies

There are also private financing institutions that have the required credit license to run a Hire-Purchase Facility, and often referred to as In-House loan.

The few reasons that make them superior to banks, is that you are able to secure a higher loan %, pushing down the upfront down-payment cost, paying a higher monthly instalment in return.

Additionally, if you are looking to get a more expensive house that can only be financed by the bank, or perhaps getting a higher HLE (HDB LOAN ELIGIBILITY) amount, as opposed to getting a bank loan for your car which impacts your TDSR (Total debt servicing ratio), you can choose to go In-House financing, which has no impact on your TDSR.

Next, the criteria which these credit companies use to assess your loan eligibility is much more lax as compared to the banks, so it’s definitely easier to secure a vehicle loan.

Of course, with the pros, comes the cons. In-house finance companies charge a higher interest rate & admin fee, typically starting from 2.98% onwards, which is a tad higher than the banks.

Balloon Scheme

While shopping for your dream car, you might have come across auto dealers offering another kind of auto loan, known as balloon scheme. This scheme is only available for cars that are still within their initial 10 years of COE, with the Preferential Additional Registration Fee (PARF) value intact.

Depending on your vehicle’s OMV, ‘OMV <S$20,000’ or ‘OMV >S$20,000’, Banks are able to loan you up to 70%/60% of the vehicle price, and if you are going for an expensive car, not only will your upfront down-payment be hefty, your monthly instalments will also be less affordable.

Conventional Car Loan

The interest for a normal car loan from most banks ranges from 2.5 to 3%.

Assuming the interest rate is 2.5% and a loan of S$60,000, your total interest payable for a 5-year loan tenure would be:

(S$60,000 x 2.5%) x 5 years = S$7,500

For a 5-year loan, the total loan amount including interest you have to pay is:

S$60,000 + S$7,500 = S$67,500

Your monthly instalment for 5 years (i.e. 60 months) is:

S$67,500 / 60 = S$1,125

Balloon Payment Scheme

Now compare the above figures with that of a balloon payment scheme.

Under this scheme, the PARF value plays a part in the loan calculation. For illustration purposes, let us put the PARF value at S$10,000.

The interest for this scheme is usually higher than a typical car loan. Assuming the interest rate is 3.75% and a loan of S$60,000, your total interest payable for a 5-year tenure would be:

(S$60,000 x 3.75%) x 5 years = S$11,250

The total loan amount that includes interest but excludes the PARF value is:

S$60,000 + S$11,250 – S$10,000 = S$61,250

Your monthly instalment for 5 years (i.e. 60 months) is:

S$61,250 / 60 = S$1,020

By comparing just between the conventional car loan & balloon scheme, the monthly instalment amount is noticeably lower on the balloon scheme, however, the catch is that under the balloon payment scheme, your last loan instalment will include the PARF rebate portion. This means the total repayment amount for that month would be S$11,020 (S$10,000 + S$1,020).

Assuming you would like to forfeit the vehicle at the last month, you can surrender the car back to the finance company, and you will only have to make your last monthly instalment as per normal.

Alternatively, if you want to sell your car at the best available price. Check out our best car dealers we recommend.